Biopharma buyers continue to shift deal-making spending away from M&A

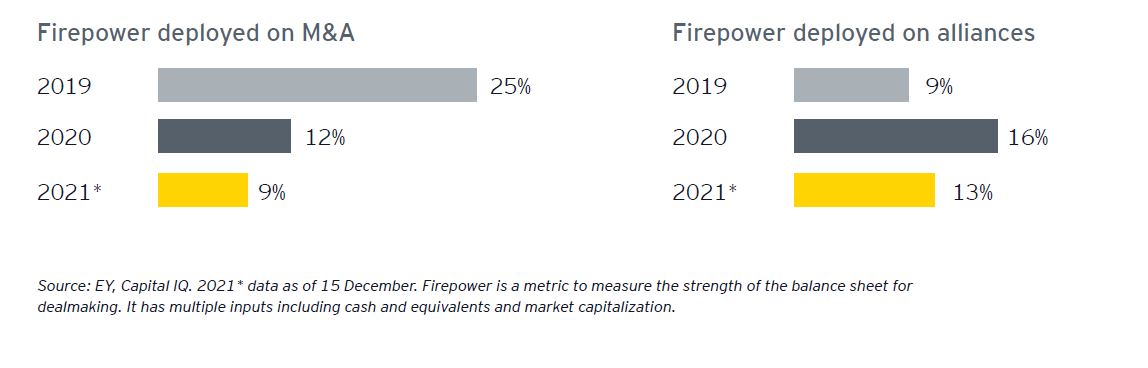

In 2021, the biopharma industry’s M&A Firepower, defined as the capacity to conduct acquisitions based on the strength of the balance sheet, reached heights not seen since 2014.

And while the pace of deal-making accelerated in the latter half of the year, the findings in the 2022 EY M&A Firepower report show a significant shift in capital allocation away from M&A.

“To stay competitive, bigger biopharma companies have no choice but to be aggressive in their pursuit of external innovation.

“But, as became clear in 2021, those transactions won’t necessarily be acquisitions. Since the beginning of 2020, major biopharmas have deployed roughly 1.5 times more Firepower on alliances relative to M&A.”

However, EY research suggests investments in alliances and partnerships did not go far enough in 2021.

“The potential deal value for alliances in 2021 did not, ultimately, match 2020. While biopharmas invested more than US$11bn upfront on 273 partnerships in 2021, EY research shows that these alliances were smaller investments focused on hedging development risk. In contrast to 2020, when there were more than 38 deals with greater than US$100m upfront, through 15 December 2021, there were only 31. Average upfront payments fell nearly US$30m year-on-year.”

2021 partnerships highlights

Noteworthy examples of strategic partnerships and alliances that were especially important for accessing new modalities in 2021 include the following:

Cell and gene therapy

Takeda/Poseida: eight in vivo gene therapies

Genentech/Adaptimmune: commercialization of allogeneic cell therapies in oncology indications

AbbVie/REGENXBIO: one-time gene therapy for wet AMD

Next-gen antibodies

Amgen’s acquisitions of Teneobio and Five Prime

BMS/Eisai: US$3b for antibody-drug conjugate

J&J/Xencor: Alliance for Phase I bispecific for B-cell cancers

RNA-based therapies

Sanofi creates center of excellence with Translate Bio and Tidal Therapeutics buys

Moderna inks multiple collaborations to manufacture its COVID-19 vaccine

Protein degradation

Pfizer/Arvinas: US$650m u/f plus equity

Eli Lilly/Lycia: US$1.6b for five protein targets

Novartis/Dunad: US$1.3b for up to four targets

Alliances are another means to offset risk, noted the analysts. They give both parties an opportunity to mutually demonstrate value earlier in their relationship, they added.

“Bigger biopharmas can familiarize themselves with newer technologies and get comfortable with the level of scientific risk involved, while smaller companies gain insights into their bigger partners’ operations, culture and capabilities.”

Achieving that shared understanding prior to an alliance is critical, says Belén Garijo, CEO of Merck KGaA, headquartered in Darmstadt, Germany, who is cited in the report.

“That is why we rigorously assess the cultural fit of organizations we partner with as part of our due diligence process,” she said.

Smaller companies must be resourced sufficiently, though, to make progress and operate as a genuine innovation engine, without simply becoming a captive of the larger company. Yet, if biopharmas can address these challenges, the rewards of partnerships are in plain view, said the EY experts.

Alliances may also give companies a pathway to future M&A, though that, historically, is the exception, not the rule, they said.

“Recent examples of the strategy include Pfizer’s 2020 acquisition of Array BioPharma and Sanofi’s 2021 purchase of Translate Bio. The latter deal originally began as a collaboration in 2018 and culminated in an acquisition when Sanofi decided it was time to establish an RNA center of excellence.”

ROI higher from alliances than acquisition

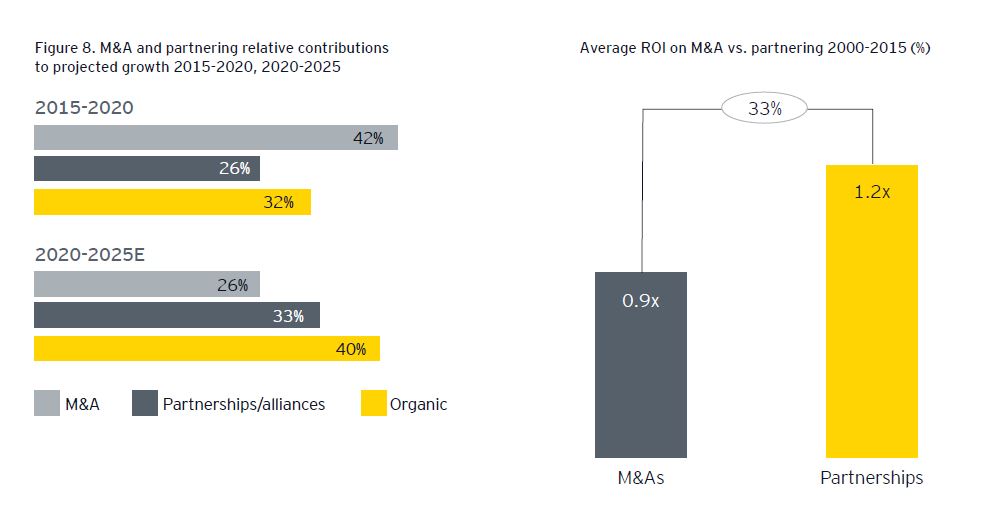

The data also suggests that when companies deploy capital toward partnerships rather than M&A they are rewarded with a greater return on their investment.

“Indeed, EY research shows that the historical return on investment (ROI) for partnerships and alliances is 33% higher than for M&A. Given this data, it’s not surprising that the EY analysis projects them playing a greater role than M&A in driving market share for leading biopharmas through 2025.”

Divestment trend

And, as companies increasingly recognize that ownership is not obligatory, divestments also gain in appeal, according to the pharma market specialists.

“The data suggests that total shareholder returns (TSR) are higher for companies that divest; however, given current fragmentation in the industry, it’s also true that biopharmas have not done enough to proactively focus their business models. Indeed, the total disclosed value of divestitures through 24 November 2021 was only US$11bn.

“In 2022, we are likely to see even more focus on divestitures.

"In November 2021, Johnson & Johnson announced plans to spin-off its Consumer Health division, mirroring recent consumer health divestitures executed by Pfizer, GlaxoSmithKline and Merck. Outside the consumer space, spin-offs of generics businesses are another area to watch.”

M&A deals

The total value of biopharma M&A in 2021 is one of the lowest on record, commented the EY team. The US$108bn total was roughly 40% of the value of biopharma M&A in 2019, they noted.

That doesn’t mean 2021 wasn’t an active year for M&A, they said.

Deal volume increased year-on-year, as biopharma majors opted for smaller bolt-ons rather than transformative M&A opportunities. In all, bolt-on deals represented 88% of total deal volume in 2021. “Betting on bolt-ons was a clear signal of biopharma companies’ appetite for less risky deals.”

Looming patent cliff

The EY research also revealed that a looming patent cliff will increase urgency for biopharmas to acquire future innovation externally, particularly in new modalities set to be key growth drivers over the next five years.

“Speed is critical to success in biotech, where obsolescence rates are increasing at an unprecedented pace,” noted Dr Garo Armen, CEO of immuno-oncology company, Agenus, in an interview for the report; May 2021 saw Agenus and Bristol Myers Squibb (BMS) set up a licensing deal for Agenus' anti-TIGIT antibody with BMS providing US$200m in an upfront payment.

The good news for major biopharma companies, continued the EY report, is that sales of newly launched products between now and 2026 will more than offset sales lost to patent expirations based on forecasts from Evaluate Pharma.

“Moreover, EY research indicates that a significant percentage of these revenues are forecast to come from biologics (43%) or new modalities (17%), including cell and gene therapies and RNA-based treatments in therapy areas that have historically had greater pricing flexibility.”

New modalities to watch

Multiple technologies have matured to make personalized therapies a growing reality, reads the report.

“Of the critical platform technologies that have come of age, cell and gene therapy is a front‐runner, with 1,800 products already in the clinics. RNA-based therapies are also rapidly gaining prominence in the wake of COVID‐-19. Outside the Pfizer/BioNTech and Moderna COVID-19 vaccines, RNA technology underpins more than 200 products currently in clinical trials for a range of illnesses, including cancer, respiratory disease, and heart failure.”

Other new modalities gaining prominence include next-generation antibodies and protein degradation technologies.

In 2021, biopharma buyers signed acquisitions and alliances potentially worth more than US$32bn to gain access to newer antibodies, especially antibody-drug conjugates that are designed to increase the power of traditional antibodies by linking them to cell-killing agents, commented the analysts.

In the protein degradation space, four companies have raised nearly US$800m in IPOs since 2020, with further validation coming from deals with companies such as Pfizer, Eli Lilly and Novartis, remarked the EY team.

For bigger biopharmas, the analysts believe there is increasing pressure to partner with or acquire startups with these capabilities, and to adapt business models to deliver these personalized products and accompanying diagnostics and services.